Michael Hiltzik: Trump's Venezuelan oil adventure is coming apart at the seams

Published in Op Eds

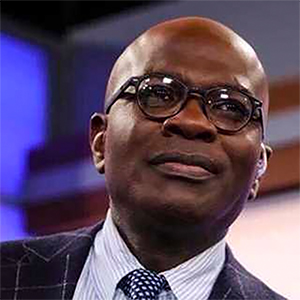

Darren Woods is known mostly as the chairman of ExxonMobil, the largest U.S. oil company. On Friday, however, he made noise in a different sphere by placing an obscure financial term into the political lexicon: "Uninvestible."

That's how Woods described Venezuela — more specifically, Venezuela's oil industry. His remark came during a meeting of some two dozen oil executives convened at the White House by President Trump, whose goal was to collect their praise for his capture and arrest of Venezuelan strongman Nicolás Maduro to face U.S. drug trafficking charges.

Trump opened the session with a lengthy spiel suggesting that the spigots of Venezuelan oil would soon be open, flooding the market with cheap petroleum for the benefit of American taxpayers, Venezuelan citizens and big oil companies.

He spoke with the confidence of a self-appointed Venezuelan shogun — indeed, over the weekend he amended his biography on his TruthSocial online platform to give himself the title of "Acting President of Venezuela."

Trump told the gathered executives that the U.S. would somehow control which oil companies would be permitted to invest in Venezuela — "We're going to be making the decision as to which oil companies are going to go in — that are we're going to allow to go in. ... You're dealing with us directly. You're not dealing with Venezuela at all. We don't want you to deal with Venezuela."

Leaving aside that Trump's authority to make those judgments is questionable in the extreme, so is the oil industry's interest in piling into Venezuela. At current world oil prices hovering around $60 per barrel or less, large investments in the Venezuelan oil fields would be marginally profitable at best. The addition of a large new supply from Venezuela, which is thought to have the largest untapped reserves in the world, would only drive the price lower.

At Friday's roundtable, Woods was the most outspokenly pessimistic about reinvesting in Venezuela, but his remarks corresponded to a new atmosphere in Trump's relationships with American institutions: resistance.

Most recently, Federal Reserve Chair Jerome Powell responded forcefully to the disclosure that Trump's hand-picked U.S. attorney in Washington, D.C., Jeanine Pirro, served subpoenas pointing to a criminal investigation of Powell and the Fed — ostensibly over the cost of renovations at the Fed's Washington headquarters.

On Sunday, Powell issued a written and video statement pushing back: "This new threat is not about my testimony last June or about the renovation of the Federal Reserve buildings," he said. "The threat of criminal charges is a consequence of the Federal Reserve setting interest rates based on our best assessment of what will serve the public, rather than following the preferences of the President."

Remarkably, Powell received support from Sen. Thom Tillis, R-N.C., who sits on both the Senate Banking and Judiciary committees, which oversee the Fed and the Department of Justice, respectively.

"If there were any remaining doubt whether advisors within the Trump administration are actively pushing to end the independence of the Federal Reserve, there should now be none," said Tillis, who is not running for reelection. "It is now the independence and credibility of the Department of Justice that are in question."

He said he would oppose confirmation of any nominee to the Fed board — including a looming nomination to succeed Powell — "until this legal matter is fully resolved." Powell's term as Fed chair ends in May, though his term as a Fed board member won't expire until 2028.

Tillis' concern was echoed Monday by another Republican senator, Lisa Murkowski of Alaska, who called the administration's Fed investigation "nothing more than an attempt at coercion." She said Tillis "is right in blocking any Federal Reserve nominees until this is resolved."

Venezuela was one subject on which some Republican lawmakers have voted to thwart Trump: Five Republican senators joined Democrats to advance a measure that would require Trump to obtain congressional approval for any further military action in the country. And 17 GOP House members joined Democrats in passing a bill extending Affordable Care Act premium subsidies for three years, despite Trump's explicit opposition to the extension. The fatal shooting of Renee Nicole Good by an Immigration and Customs Enforcement agent in Minneapolis has drawn bipartisan criticism.

In the past, Trump's threats and demands have yielded almost instantaneous assent from the business leaders he has targeted. The oil industry roundtable was notable for the participants' lukewarm endorsement of Trump's expectation for a wholesale return to Venezuela.

The most enthusiastic attendee was Mark Nelson, the vice chairman of Chevron, the only U.S. oil company to remain in Venezuela after the country nationalized the oil industry in 1976. He said Chevron was poised to sharply increase its output of Venezuelan oil.

Others made optimistic noises but not explicit commitments. Harold Hamm, the founder and chairman of the fracking and shale oil company Continental Resources, whom Trump effusively praised during the session, demurred when Trump asked him if Continental would plunge into the Venezuela market.

"It's got its challenges," Hamm said. Continental is chiefly a domestic producer; it has some ventures in Turkey, but isn't known as an international producer.

"Our giant oil companies will be spending at least $100 billion" to rebuild the Venezuelan industry, Trump said.

That's the assertion that drew Woods' rebuke. He noted that the assets of Exxon (which merged with Mobil in 1998) had been seized twice since they first entered the country in the 1940s.

"So you can imagine that to reenter a third time would require some pretty significant changes. ... If we look at the legal and commercial constructs and frameworks in place today in Venezuela, today it's uninvestible, and so significant changes have to be made."

By asserting that the U.S. would dictate which companies would be invited to invest in Venezuela, Trump may have injected further uncertainty into oil companies' judgments about the wisdom of the venture.

Among other concerns, any investment starting now wouldn't yield profit for several years, probably not before Trump leaves office. That raises doubts about who would be the government counterparty to any deal and who would guarantee the safety and stability of the investment. The U.S.? A reconstituted Venezuelan regime?

Trump himself underscored those doubts on Sunday, when he told reporters traveling with him that he was "inclined" to keep ExxonMobil out of Venezuela out of pique at Woods' comments. "I didn't like Exxon's response," he said. "They're playing too cute."

At the Friday meeting, Trump's comments about the history of American investment in Venezuela were confused and confusing. As I reported earlier, prior to the capture of Maduro, he alluded to the 1976 nationalization by demanding "the return to the United States of America all of the Oil, Land, and other Assets that they previously stole from us."

He repeated the assertion Friday, stating "decades ago, the United States built Venezuela's oil industry at tremendous expense. ... Those assets were stolen from us."

The truth is that American and other foreign companies operated in the Venezuelan oil fields as concessionaires, granted rights to extract, refine and ship oil that was a Venezuela-owned resource.

Several oil companies sought compensation through international tribunals and arbitrators. ExxonMobil received $908 million from arbitrators in 2012. In 2018, arbitrators awarded ConocoPhillips $2 billion, a second arbitration panel awarded the company an additional $8.7 billion in 2019 and a third panel awarded it $33 million. These made the company what its chairman, Ryan Lance, said at the Friday meeting into "the largest non-sovereign credit holder in Venezuela today." Both companies were evicted from the country in 2007 by Maduro's predecessor, Hugo Chávez.

ConocoPhilips said in its most recent disclosure for the quarter ended Sept. 30 that it had received $793 million of those awards and that collection actions for all three are "ongoing."

But at Friday's meeting, Trump told Lance not to expect the U.S. government's help in recovering any of that money. "You'll get a lot of your money back," Trump said. "We're going to start with an even plate, though. We're not going to look at what people lost in the past. ... You're going to make a lot of money but we're not going to go back." The same day as the meeting, Trump issued an executive order prohibiting any creditors from recovering any of their claims from money the U.S. government collects from the sale of Venezuelan oil.

When Lance said that his company had lost $12 billion in Venezuela, Trump said: "Well, good write-off." Lance responded: "It's already been written off." The company wrote off $8.5 billion from its Venezuela investment in 2007.

ConocoPhilips told me that Lance "appreciates the valuable opportunity to engage with President Trump in a discussion about preparing Venezuela to be investment-ready." ExxonMobil didn't respond to my request for information about its claims.

There are signs that conditions in Venezuela are destined to get worse before they get better — or at least that Trump's military action and capture of Maduro hasn't restored social or political stability to the country.

On Saturday, the U.S. Embassy in Caracas warned U.S. citizens not to travel to Venezuela and any citizens currently in the country to "leave the country immediately." The embassy cautioned that "there are reports of groups of armed militias, known as colectivos, setting up roadblocks and searching vehicles for evidence of U.S. citizenship or support for the United States."

Indeed, the unrest in Venezuela appears to be general. Hopes that Maduro's ouster would precipitate a return to democracy have been dashed, at least in the near term, as the government is now led by Maduro's vice president, Delcy Rodríguez, and the paramilitary colectivos are reportedly confronting Venezuelan citizens on the streets, not just Americans. The wait for an "investible" Venezuela may be a longer one than Trump anticipated.

____

©2026 Los Angeles Times. Visit at latimes.com. Distributed by Tribune Content Agency, LLC.

Comments